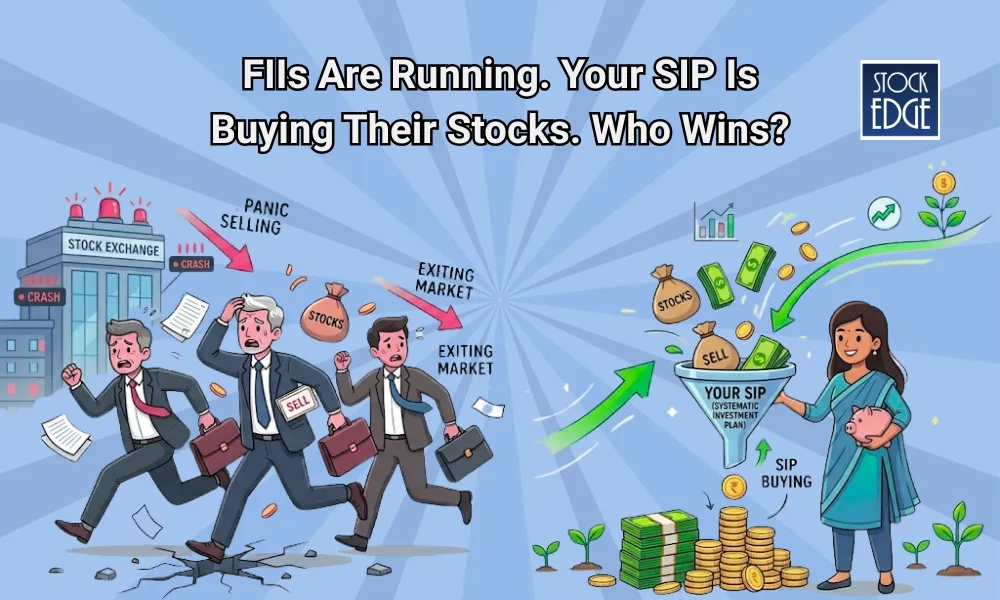

The Indian banking sector has long been the favorite playground for Foreign Institutional Investors (FIIs). However, April 2026 marked a significant shift in the narrative. While the headlines were dominated by a staggering ₹70,000 crore exodus by foreign funds, the Bank Nifty didn't crumble. Instead, it showcased a level of resilience that would have been unthinkable a decade ago.

The reason? The "Great Wall" of Domestic Institutional Investors (DIIs). Here is an analysis of this institutional tug-of-war and what it means for the person sitting behind a retail trading terminal.

The FII Exodus: Why the "Smart Money" is Leaving

Historically, FIIs were the primary drivers of volatility in the Bank Nifty. In April 2026, several global factors converged to trigger a massive sell-off:

- The Yield Gap: Rising U.S. Treasury yields have made emerging markets look riskier, prompting a flight to "safe haven" assets.

- Geopolitical Friction: Ongoing tensions in the Strait of Hormuz have pushed oil prices toward the $115 mark, directly threatening the margins of Indian banks.

- Currency Pressure: With the Rupee hovering near 95.00 against the Dollar, FIIs are protecting their returns against currency depreciation.

The DII Shield: The New Power Center

If FIIs are the "fair-weather friends" of the Indian market, DIIs that are comprising mutual funds, insurance companies, and pension funds have become the bedrock. For every crore the FIIs pulled out in April, domestic funds were there to absorb the impact, fueled by the relentless engine of Systematic Investment Plans (SIPs).

FII vs. DII: A Comparison of Philosophies

| Feature | Foreign Institutional Investors (FII) | Domestic Institutional Investors (DII) |

| Primary Driver | Global macro trends & dollar strength. | Domestic liquidity & retail SIP inflows. |

| Time Horizon | Often tactical and short-to-medium term. | Structurally long-term. |

| Impact on Bank Nifty | Triggers sharp, news-based volatility. | Provides "price floors" during crashes. |

| April 2026 Action | Net Sellers (₹70,000 Cr+). | Aggressive Net Buyers. |

The Power of SIPs: Creating a "Permanent Bid"

The massive cushion we are seeing in 2026 is fueled by the relentless compounding of retail Systematic Investment Plans (SIPs).

- The "Permanent Bid": Retail SIPs act as a structural "permanent bid" in the market. Every month, billions of rupees automatically flow into mutual funds, regardless of whether the headlines are good or bad.

- Counter-Cyclical Force: This constant influx gives fund managers a massive cash pile to buy the dips when FIIs are selling, effectively preventing the liquidity voids that used to cause historic market crashes.

"Hot Money" vs. "Patient Capital"

To help readers understand the core philosophy difference, contrast the nature of their capital:

- FIIs run on "Hot Money": Foreign capital is highly momentum-driven. It operates on global macro arbitrage that is swapping countries or asset classes at the click of a button based on US Treasury yield spreads or currency fluctuations.

- DIIs run on "Patient Capital": Domestic institutions like mutual funds, insurance companies (LIC), and pension funds (EPFO) are structurally obligated to invest in the domestic economy. They don't have the luxury or the mandate to panic-shift their capital to Wall Street or Tokyo when things get volatile. They are "missionary investors" rather than mercenary ones.

Why the Index Remains Resilient

The Bank Nifty’s ability to hold its ground despite the FII onslaught is a testament to the maturation of the Indian market.

In the past, a ₹70,000 crore FII sell-off would have triggered a 15–20% correction in the banking index. In 2026, we are seeing "controlled descents" and quick recoveries. This resilience is driven by the fact that the ownership of the Indian market is shifting. Domestic capital is no longer just a "participant"; it is increasingly the price-setter.

The Structural Shift: We are witnessing a transition from a market dependent on foreign sentiment to one fueled by domestic savings. This reduces the "beta" (volatility) of the Bank Nifty relative to global shocks.

What This Means for Long-Term Retail Investors

For the individual investor, this institutional tug-of-war can be noisy, but the signal is clear: The floor is getting stronger.

- Lower Correlation with Global Markets: While the Bank Nifty will still react to the Fed or oil prices, the "panic-selling" phase is often short-lived because DIIs view these dips as buying opportunities.

- Focus on Fundamentals: With FIIs out of the way in certain pockets, stock prices are beginning to align more closely with earnings rather than just "flow-based" momentum.

- Patience is a Competitive Advantage: Retail investors often get caught in the crossfire of institutional selling. The lesson from April 2026 is that if the underlying banking business (like credit growth and NIMs) remains healthy, the "sell-off" is merely a transfer of shares from foreign hands to domestic ones.

A Striking "Then vs. Now" Comparison

- In 2013: A net FII inflow of around ₹9,428 crore per month was enough to dictate the entire direction of the Indian market.

- In 2026: The Indian market is routinely absorbing FII outflows of over ₹1,000,000 crore (₹1 lakh crore+) in a single month without throwing the broader system into a panic.

- The Takeaway: The velocity of selling that would have crippled the market a decade ago is now being cleanly absorbed by domestic liquidity.

The Verdict: Who Wins?

In the short term, the FIIs "win" by moving the needle and creating exit liquidity. However, in the long term, the Indian Retail Investor who are represented by the DIIs, is winning the battle for ownership of India's financial future.

As the Bank Nifty navigates the 55,000-level, the tug-of-war continues. But for the first time, the rope isn't just moving in one direction.

This article is for informational and educational purposes only and does not constitute financial advice. Please consult with a SEBI-registered financial advisor and conduct your own thorough research before making any investment decisions.

Sign in to leave a comment.